If you have received a notice from the IRS asking for Form 433-A and are unsure what it is, you’re not alone.

Many taxpayers panic when the IRS asks them for this financial disclosure form. But filling out Form 433-A is the tool that helps the IRS understand your financial condition when you’re in tax debt.

However, one small mistake can slow things down or lead to a rejected offer. But don’t worry—we’ve got you covered.

In this blog, we will break down Form 433-A step by step, explain what the IRS is really looking for, guide you through every part of it, and help you complete it with confidence.

What is Form 433-A?

| Form 433-A is officially called the IRS Collection Information Statement, used by individuals and self-employed people who owe back taxes. It’s a financial disclosure form for IRS used when a taxpayer owes the IRS but can’t pay the full tax amount at once. |

It provides the IRS with a complete picture of your financial life, like your income, expenses, assets, debts, and more

This form helps the IRS decide:

- If you qualify for a payment plan

- If you are dealing with a financial hardship

- If you are eligible for an offer in compromise

- Determine if your case should be marked as Currently Not Collectible

- Evaluate you for a Partial Payment Installment Agreement (PPIA)

Who Should Complete Form 433-A?

You should fill out the 433 A form if:

- You owe back taxes and want a long-term payment plan

- You are self-employed or a sole proprietor

- Apply for IRS tax debt resolution form options like OIC

- Are personally liable for business taxes (like the Trust Fund Recovery Penalty)

- Own a disregarded entity like an LLC taxed as a sole proprietorship

- Are involved in a tax dispute handled by a revenue officer

- Or the IRS specifically requests it

The IRS uses your form to see if you qualify for programs like Offer in Compromise or Currently Not Collectible status.

If you’re a wage earner and don’t own a business, you may still need this form if your debt is large.

| Note: If you’re only dealing with smaller tax debts or basic payment plans, the IRS may instead ask for Form 433-F. |

How to Complete Form 433-A?

IRS Form 433-A instructions can be confusing at first. The form has 7 sections. But not everyone fills out all the parts.

| Who | Sections to Complete |

| Wage Earners | 1–5 |

| Self-Employed | 1, 3–7 |

| Wage Earner + Self-Employed | 1–7 |

Some parts ask for personal details. Other parts ask about your income, debts, and business (if you have one).

Required Documents to AttachHere’s what you should send with your 433A:

|

Now let’s go through the sections step by step.

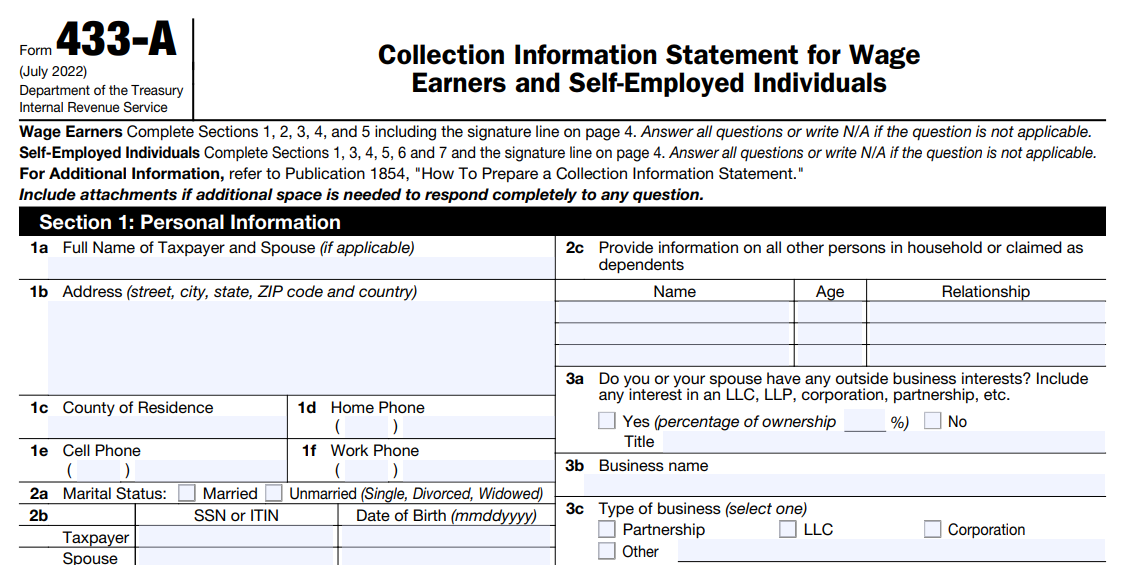

Form 433-A Section 1: Personal Information

This section collects basic details:

- Name, address, SSN or ITIN

- Date of birth

- Marital status

- Contact info

- Number of dependents

- Business ownership details (if any)

Also, list your spouse’s name and info if you file taxes together. Include it, even if you’re separated or divorced but still filing jointly.

Bonus Read → Social Security: Maximizing Benefits for Spouses

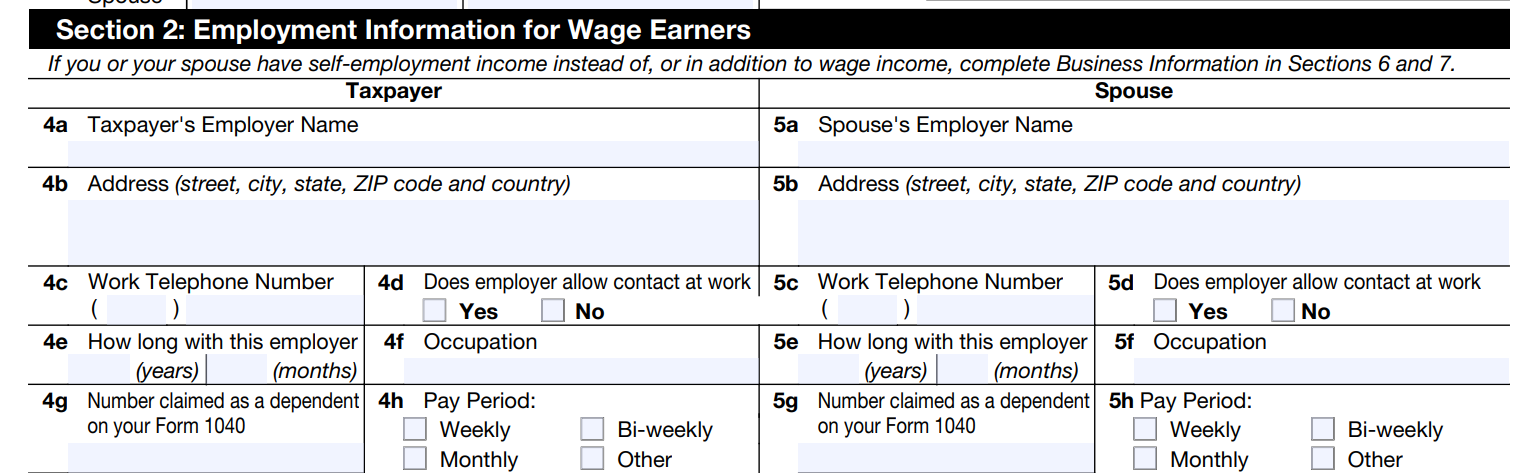

Form 433-A Section 2: Employment Information for Wage Earners

This section wants to know where you work. If you’re a wage earner, you need to give:

- Employer name and address

- Job title

- How long you have worked there

- How often you get paid (weekly, bi-weekly, monthly)

- Whether your spouse is employed and their details

You’ll also need to provide your last pay stub. If you’re unemployed, write that down clearly.

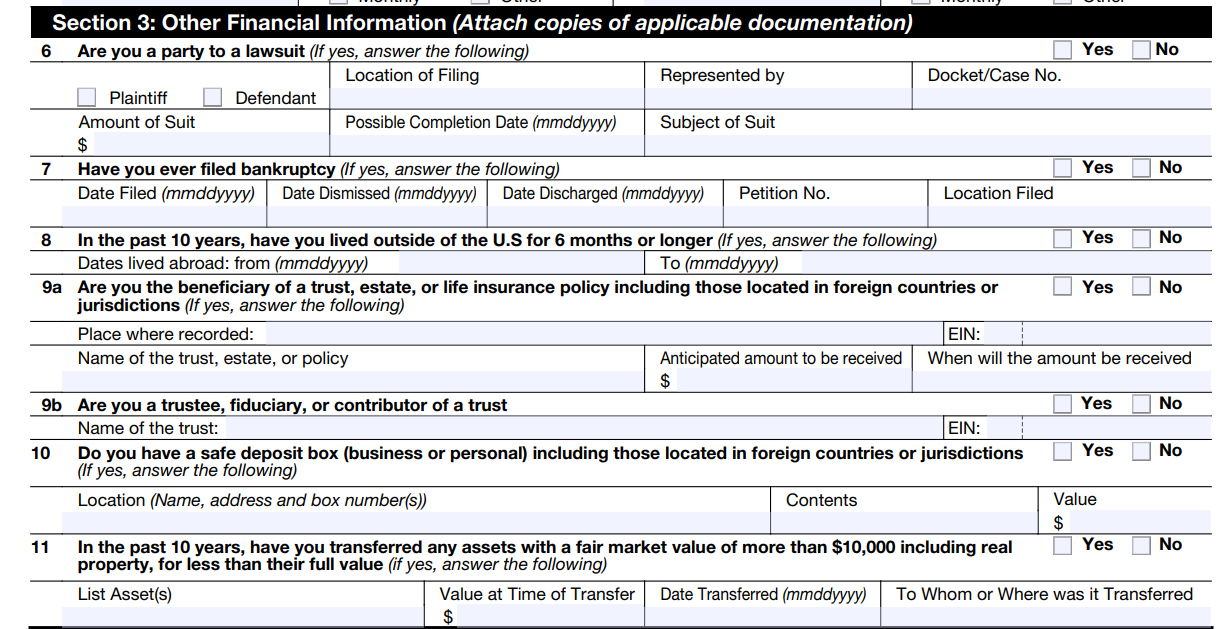

Form 433-A Section 3: Other Financial Information

This part checks your debts and legal issues.

It asks:

- Are you involved in a lawsuit?

- Do you owe child support or alimony?

- Have you filed for bankruptcy?

- Do you expect to get money from someone else?

- If you’ve lived outside the U.S. in the last 10 years

- Whether you’re a trust beneficiary

- Details of any safe deposit boxes

- Any large asset transfers over the past decade

Be honest. The IRS uses this information to determine whether other people or courts are already taking your money.

Form 433-A Section 4: Personal Asset Information

Most people feel overwhelmed by this section, as it is long and asks you to list everything you own.

Let’s break it down:

Bank Accounts

List all checking, savings, and money market accounts. Include:

- Bank name

- Account number

- Current balance

The IRS wants to know if you’re hiding money. Even if your account has $50, include it.

Know More → Bank Levies Unveiled: Can the IRS Take Your Money And How to Stop Them?

Investments

List stocks, bonds, retirement accounts (401(k), IRA), or mutual funds. Include their current values.

Bonus Read → Decoding Retirement Taxes: Roth IRA, 401(k), and More

Virtual Currency

Do you own crypto like Bitcoin or Ethereum? Write down what you own and its value in U.S. dollars.

Business Interests

Own shares in a private business or partnership? List that here.

Available Credit

Mention credit cards and lines of credit. The IRS checks to see if you’re borrowing money.

Cash Value in Life Insurance

It might have a cash value if you have whole or universal life insurance. Term life doesn’t count.

Real Property

List your home or other real estate.

- Address

- Market value

- Mortgage balance

- Monthly payment

Read More → Mastering Property Tax Planning: A Guide to Smarter Finances

Personal Vehicles

Include all cars, trucks, motorcycles, boats, and RVs. Write down their value and loan balance (if any).

Personal Assets

Add items like

- Jewelry

- Furniture

- Firearms

- Electronics

Even if the value is low, list it. The IRS just wants a complete picture.

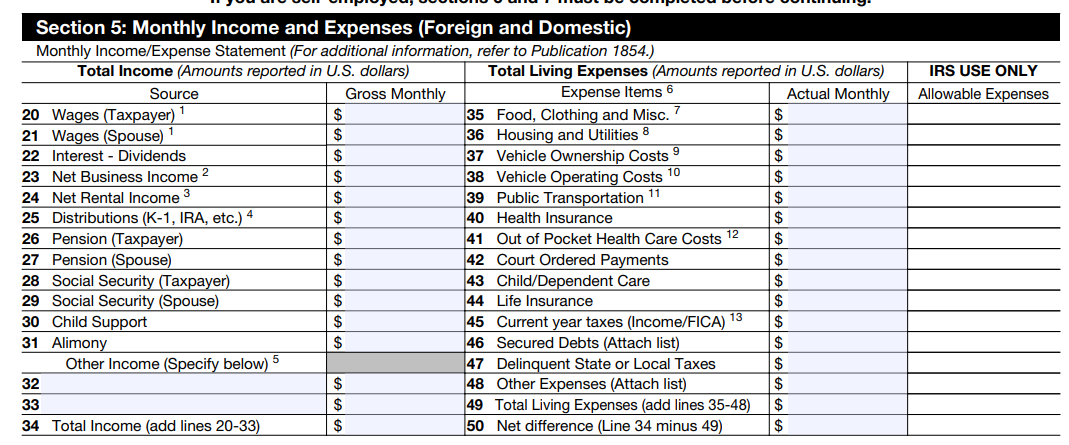

Form 433-A Section 5: Monthly Income and Expenses

This is the most crucial section. Here, you’ll share:

- How much you earn monthly (wages, self-employment, social security)

- How much you spend (rent, food, utilities, transport)

If your expenses are too high, the IRS may challenge them.

Make sure your numbers are accurate and provable. Attach receipts and statements when possible.

This section helps the IRS calculate how much you can afford to pay them monthly and determine IRS payment plan eligibility.

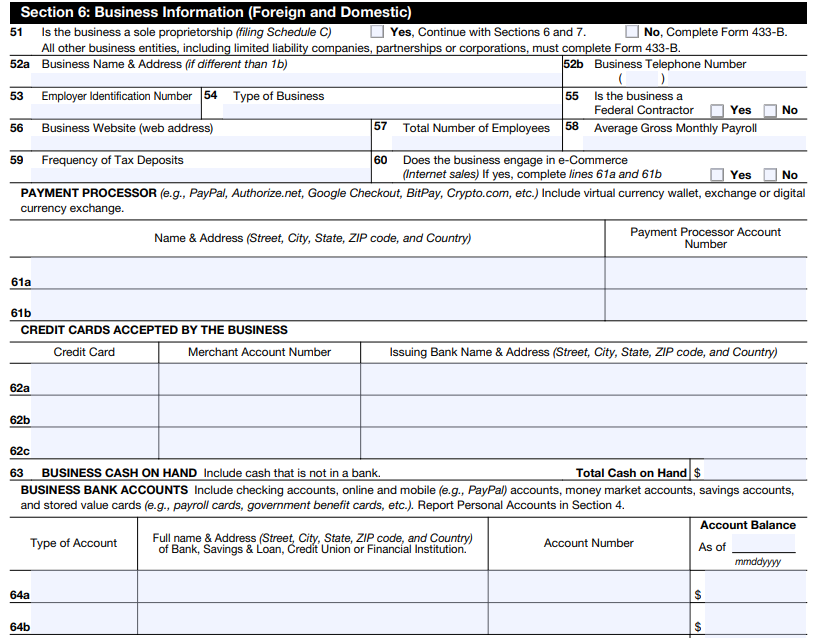

Form 433-A Section 6: Business Information (Self-Employed)

This is for self-employed people or business owners.

You’ll be asked to fill in:

- Include the business name, type, address, number of employees, and your EIN

- Provide gross monthly payroll and e-commerce/payment platform details

- List business assets, accounts receivable, and outstanding debts

Attach:

- Bank statements

- Profit & loss statement

- Tax returns

The IRS uses this to see if your business is making money.

Bonus Read → Tips for Effective Business Tax Preparation

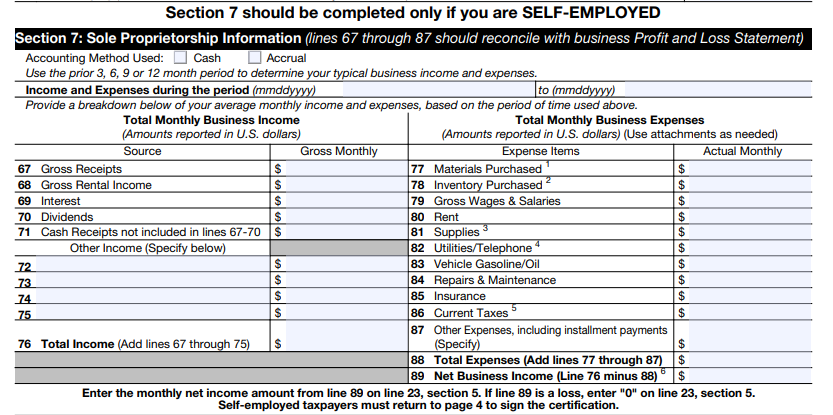

Form 433-A Section 7: Sole Proprietorship Information

If you own a small business under your own name (no LLC or Corp), this section is for you.

It asks:

- Do you take a regular draw (payment)?

- What’s your role in the business?

- Do you share ownership?

- Operating costs like rent, supplies, wages, and utilities

- Total net income

This tells the IRS if your business can contribute to tax debt payments.

Also Read → Key Changes Affecting Small Business Employers

How the IRS Uses Your Form 433-A?

Once submitted, the IRS uses your form to:

- Calculate how much you can realistically pay toward your tax debt (this is called your Reasonable Collection Potential or RCP)

- Decide whether to accept a payment plan, OIC, or declare you Currently Not Collectible

- Review if your financial disclosure supports penalty abatement or another IRS financial hardship tax relief plan

If you underreport, round numbers, or forget assets, the IRS may think you’re dishonest. This can lead to your request being rejected.

Common Versions of Form 433-A

There are different versions of this form, and it’s important to know which to use:

- Form 433-A: Standard, long-form financial disclosure.

- Form 433-A (OIC): A special version for those applying for an Offer in Compromise. It’s focused on assets and disposable income.

- Form 433-F: A short version used when less detail is needed.

- Form 433-B: Used by businesses, not individuals

Form 433-A Versus Form 433-F

Form 433-A vs. Form 433-F – What’s the difference?

The table below shows the differences between Form 433-A and Form 433-F

| Feature | Form 433-A | Form 433-F |

| Length | Long and detailed | Short and simple |

| Used for | Larger tax debts, Offer in Compromise | Smaller tax debts |

| Who fills it out | Wage earners, self-employed, sole proprietors | Mostly wage earners |

| Includes business info | Yes, detailed info about income & expenses | No |

| Real estate & assets | Requires full listing | Basic or none |

| Required by | Revenue Officers (field collection cases) | Automated Collection System (ACS) |

| Time to complete | Longer, more documents are needed | Quicker to fill out |

The Form 433-A vs. Form 433-F difference primarily lies in the depth of financial info needed. The “A” form asks for more. Use the 433A form if you’re self-employed or owe a large tax bill.

Where to Download Form 433-A?

You can get IRS 433-A from the official IRS website.

Print it. Fill it out by hand. Or use a PDF editor if you prefer typing.

If you’re unsure how to fill it out, work with a tax pro who understands the IRS Collection Information Statement process.

Let Hopkins CPA Firm help you with the IRS 433-A form → Book a discovery call now!

Get Your IRS Forms Done Right with Hopkins CPA Firm

Filling out Form 433-A correctly is crucial when dealing with the IRS about unpaid taxes. A small mistake on the 433 A form can lead to delays or even rejection. However, completing it accurately can help reduce penalties and negotiate more favorable terms. That’s why working with Hopkins CPA Firm makes all the difference.

We help you complete the form accurately, explain what the IRS is really looking for, and guide you through the whole process. With our experts’ support, you won’t have to face the IRS alone. Let us help you get it right the first time.

Don’t believe us; listen to what our client says: Professional team that made me feel as if I had made the right choice, even from the beginning. Resolved my tax problem and am looking forward to using him in the future for tax preparation. — Team Prodigy |

When dealing with the IRS, trust us to handle the details and protect your interests. Contact Hopkins CPA Firm today!