An Offer in Compromise is the IRS program that lets qualified taxpayers settle tax debt for less than the full amount owed, and filing it correctly starts with understanding the rules behind Form 656.

When IRS unpaid tax has grown beyond what you can realistically pay, mistakes, missing details, or wrong expectations can quickly derail your request.

In this blog, we will explain what Form 656 is and walk you step-by-step through filling it out. By the end, you’ll know exactly how to approach this process with confidence.

What Is Form 656?

The IRS offers Form 656, also called the Offer in Compromise booklet, to help people who owe but can’t pay in full. If you qualify, you can settle for less than you owe, based on your income, assets, and ability to pay.

Here’s how it works:

- You fill out the IRS Form 656.

- You submit financial information (Form 433-A(OIC) or 433-B(OIC)).

- You send a $205 fee (unless you qualify for low-income certification).

- You offer a payment plan, such as a lump sum or a periodic one.

If the IRS accepts, you make the payments, and the rest of the debt is forgiven. It’s one of the most powerful tools in the tax world.

How to Fill Out Form 656?

Form 656 has eight sections, each asking for different details. Let’s go step by step.

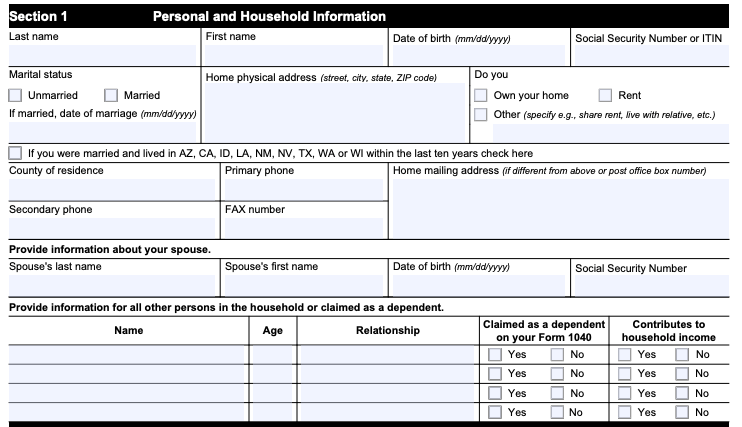

Section One: Individual Info

If you’re filing as a person (not a business), this is your basic profile section. If you don’t fill this out correctly, the IRS can’t match your offer to your tax account.

- Name, Social Security Number (or ITIN/EIN for a business).

- Enter the address, and if it’s new, enter the changed address.

- Joint filers must give both names and numbers.

- Tax periods you want the deal for, like which years you owe on.

If you qualify for the low-income certification, check the box given. That saves you the $205 fee and initial payments while your offer is under review.

Explore: Simple Steps to Change Your Address with the IRS Online

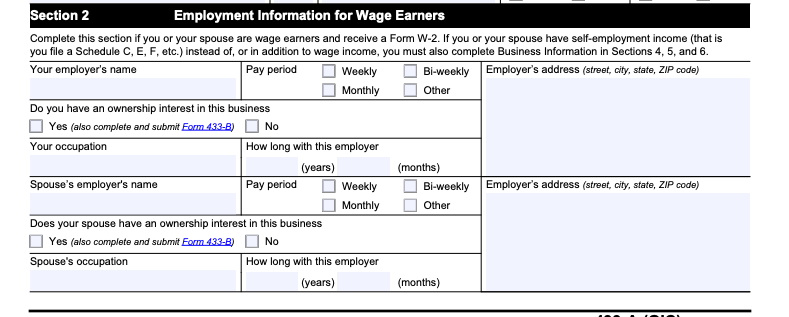

Section Two: Business Details

If the offer is for a business (like a corporation, partnership, or LLC), fill out this part. Enter the business name, Employer Identification Number (EIN), and contact info.

If you owe both personal and business taxes, you’ll need two separate offers, and that means two separate fees and payments. This section makes sure the IRS ties your offer to the right business account.

Section Three: Reason for the Offer

Here’s where you explain why you’re asking for a break. The IRS gives you three main options:

- Doubt as to Collectibility: You don’t have enough income or assets to pay the full debt. Most people use this reason.

- Effective Tax Administration – Economic Hardship: You could pay, but it would create big trouble, like not being able to meet basic needs. Only for individuals.

- Effective Tax Administration – Public Policy/Equity: Paying would be unfair, maybe because of rare and special facts, not because of hardship.

If you check economic or public policy hardship, attach a letter with details.

Section Four: Payment Terms

This is where you decide how you’ll pay for the offer. You’ve got two tracks:

- Lump Sum: You pay 20% upfront with your application, then the rest in five or fewer payments within five months of acceptance.

- Periodic Payment: You send your first month’s payment with the application, then keep making payments while the IRS reviews your offer. If they accept, you keep paying until it’s done (up to 24 months).

If you qualify for low-income certification, you can skip the upfront payment. Otherwise, the IRS expects at least something with your application.

If you don’t make those periodic payments while waiting for IRS approval, they can kick your offer back with no appeal rights.

Section Five: Designate Payments

If you want your payments to cover a certain year or kind of tax debt, say so here, such as “Put this toward payroll tax debt.” If left blank, the IRS decides. You can also use electronic payments (EFTPS or the Individual Online Account, known as IOLA).

Section Six: Source of Funds & Filing Steps

Here, you explain where the money will come from, such as using salary, savings, help from a family member, or a loan.

- If you’re mailing the offer, make the check payable to “United States Treasury.” If you’re paying online, use your IRS account or EFTPS.

- Also, don’t send original tax returns with your offer. If you filed one in the last 10 weeks, attach a copy.

- List any payments you’ve already made electronically.

Also, check off that you’ve filed all needed tax returns. Unfiled tax returns are required to be filed. If not, list the years.

For estimated taxes (if self-employed), confirm you are up to date or explain if not needed. If you mess up here, the IRS may return your offer.

Section Seven: Terms You Must Agree To

When you sign Form 656 Offer in Compromise, you’re agreeing to:

- Keep filing and paying taxes on time for the next five years.

- Give up any tax refunds for the year the IRS accepts your offer.

- Understand that your offer can be accepted, rejected, or returned.

- Know that if the IRS takes more than 24 months to respond, it’s automatically accepted (unless a court case pauses the clock).

The IRS also explains what happens if you default. If you don’t follow through, they can bring back your full debt, add interest, and file a lien again.

If the IRS rejects your offer, you have 30 days to appeal. If they “return” it for missing items, you don’t get appeal rights.

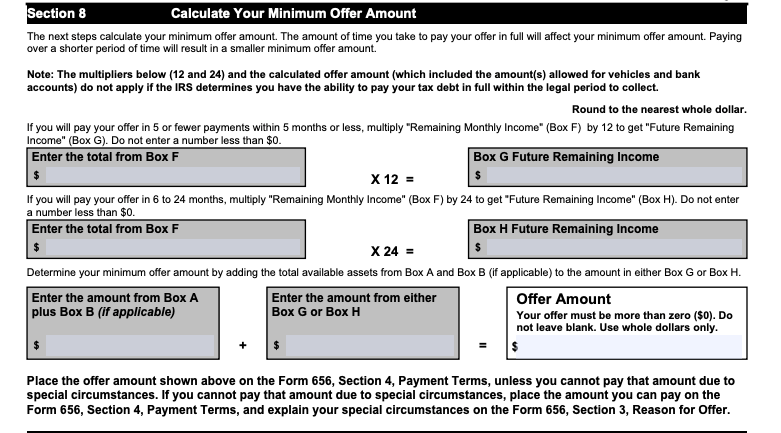

Section Eight: Signatures

This is where you confirm, under penalty of perjury, that everything you wrote is true. If filing jointly, both sign. If a paid preparer (a tax pro like a Houston CPA firm) helped, they sign too.

You also give your phone number and can check a box if you want the IRS to leave voicemails about your offer. Without a signature, the IRS won’t even look at your offer.

Other Forms in the 656 Booklet

The Form 656 booklet also includes:

- Form 433-A (OIC): For individual info such as property, debts, income, and expenses.

- Form 433-B (OIC): Same but for business filers.

- A checklist so you don’t miss documents.

- Mailing instructions (Brookhaven, NY, for some states; Memphis, TN, for others).

The booklet is your complete guide, so don’t skip reading it.

What Is Form 656-L?

If you get a tax bill you know is wrong, use Form 656-L (“doubt as to liability”). Unlike regular Form 656, you use this when you don’t trust the IRS math, not when you just can’t pay. Use it only if you truly think you owe zero (or way less).

Hopkins CPA Firm Makes Offers Work

Filing Form 656 isn’t easy for most DIY filers. Laws are tricky, and if you’re drowning in tax papers, an expert in CPA individual tax preparation is worth the investment.

Hopkins CPA Firm is the best choice when it comes to handling IRS Form 656. We review your entire financial picture and calculate a realistic offer the IRS is more likely to accept, and fight for you if there’s pushback. We are one of the top-rated Austin cpa firms.

Contact us today and let us take the pressure off your shoulders, guide you through every step, and help you win the relief you deserve.

FAQs

The purpose of IRS Form 656 is to let taxpayers settle tax debt for less than they owe. By using Form 656, you propose an affordable payment that reflects your financial reality, helping you avoid wage garnishments or aggressive collections.

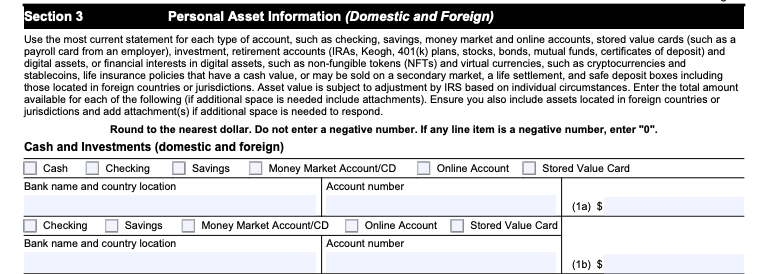

The IRS has strict rules and calculations. Use their online Pre-Qualifier Tool. Your offer is usually what you can pay after all basic living costs are met. Use your numbers from Forms 433-A (OIC) or 433-B (OIC). The IRS expects offers to reflect your real financial capacity.

Other options before using IRS Form 656:

Installment plans (pay over time, often with less stress)

Temporary delay because of hardship (IRS pauses collections)

Bankruptcy (extreme cases only)

Yes. As of 2025, most individuals can use their IRS Individual Online Account. This makes submitting and tracking offers quicker. Businesses often need to mail in the paperwork. Always check IRS updates for the latest.

The usual time is 6–9 months. If you didn’t hear back in 2 years, the IRS accepts your offer by law. Some cases move faster or slower; keep records and don’t stop payments if you’re on a plan.

Once your IRS Offer in Compromise Form 656 is settled, your stress drops. You pay as promised; if you finish all payments, the IRS lifts liens (usually within 45 days). You must then follow all tax rules, file tax returns on time, and pay all taxes for five years. Once completed, liens are released, and remaining balances are forgiven.

If your IRS offer in compromise form 656 is rejected, you can appeal within 30 days. Many taxpayers succeed at appeals by correcting errors, clarifying finances, or showing hardship. A “returned” offer, however, has no appeal rights. If your refund or paperwork was lost, try IRS Form 3911.

No. IRS Form 656 only applies to federal debts. Many states offer their own compromise programs, but they require separate paperwork. Check your state’s Department of Revenue for details, as state forms differ from IRS Form 656.