A federal tax lien on your record can crush your credit, block loans, and even hurt job or business opportunities. It follows you in background checks and makes life harder when you’re trying to move forward. However, the IRS gives you a way to pull that lien notice off the public record using a single application.

This is where IRS Form 12277 comes in. It’s the official request to withdraw a filed lien notice so you can start repairing your financial standing.

In this blog, we will explain what Form 12277 is, how to complete it, and what to expect after filing. By the end, you’ll know how to use it to clear your record and move forward.

What Is IRS Form 12277?

IRS Form 12277 is the official application you use to ask the IRS to withdraw a filed federal tax lien notice. Its full title is “Application for Withdrawal of Filed Form 668(Y), Notice of Federal Tax Lien.”

When the IRS files a tax lien notice (Form 668(Y)), it becomes part of the public record. That notice tells creditors, banks, and even landlords that the government has a legal claim on your property because of unpaid taxes, even if you’ve paid your balance or worked out a plan with the IRS; that public filing can still hurt your credit and limit financial opportunities.

Form 12277 focuses on removing the public lien notice from the record, not removing the lien from the property. If approved, the IRS will file a separate document, Form 10916(c), that officially withdraws the lien notice where it was recorded. This makes it as though the lien notice was never filed in the first place.

The Legal Basis for the Withdrawal of a Tax Lien

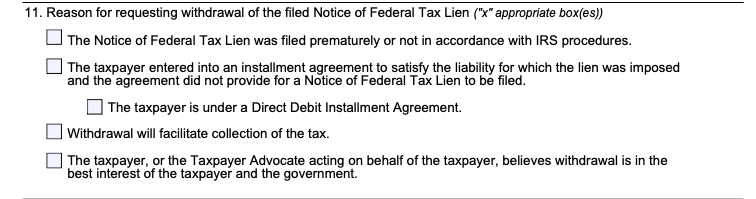

The law that lets the IRS withdraw a filed lien notice is Internal Revenue Code section 6323(j). The form cites it by name. Here are the exact reasons you can check on IRS Form 12277:

- The IRS filed the notice too soon or not under its own rules.

- You have an installment agreement, and it did not call for a lien notice.

- You are under a Direct Debit Installment Agreement.

- Withdrawal will help the IRS collect the tax.

- You, or the Taxpayer Advocate for you, believe withdrawal is in the best interest of you and the government.

How these rules work together in real life:

- Section 6323(j) is about removing the filed notice from public records. That is what IRS Form 12277 does.

- A release under section 6325(a) ends the lien itself, usually after full payment or when the lien is no longer enforceable. The form’s “Released” status mirrors that point.

The word “Released” also appears on the form. “Released” means the lien is satisfied or no longer enforceable, which is why “release” and “withdrawal” are not the same thing.

Eligibility Criteria

You can apply if a federal tax lien notice (Form 668(Y)) was filed and one of the listed reasons applies. Start by checking your lien’s current status on IRS Form 12277:

- Open: There is still a balance on the tax shown on the notice.

- Released: The lien has been satisfied or is no longer enforceable.

- Unknown: You are not sure of the status.

Pick the reason that matches your facts. Common fits on IRS tax form 12277 include a new Direct Debit Installment Agreement, a prior agreement that never called for a lien, or proof that pulling the notice will help you pay faster.

If your lien already shows “Released,” you can still request a withdrawal of the filed notice to clean the record. Attach loan pre-approvals, job letters, or other papers that show how a withdrawal helps you and helps the IRS collect.

Lien Withdrawal vs. Lien Discharge

Taxpayers often confuse a lien withdrawal with a lien discharge. Both sound similar but have different effects. Here’s a simple side-by-side breakdown so you know which one fits your case.

| Feature | Lien Withdrawal | Lien Discharge |

| What It Does | Removes the public notice of the lien (Form 668(Y)) from records. The debt may still exist. | Removes the lien from a specific property (like a home sale), while the lien can still attach to other assets. |

| Form Used | IRS Form 12277 (Application for Withdrawal of Filed Form 668(Y)) | Other IRS discharge forms (not Form 12277). |

| Effect on Debt | Does not erase the tax debt; it only clears the public filing. | Does not erase the debt; it only detaches it from one property. |

| Main Benefit | Helps improve credit reports and loan chances, and clears the lien notice from public view. | Lets you sell, refinance, or transfer specific property while a lien is still in place. |

How to Complete Form 12277?

You do not need legal jargon for this part. Follow the steps below exactly to fill out IRS Form 12277.

Your Basic Information (Sections 1–3)

The first part of the form is about you.

- Sections 1–2: Write your full name and Social Security Number (or EIN for a business). Use the exact name and number shown on the lien notice (Form 668(Y)).

- Section 3: If someone fills out the form for you, list their name. For businesses, add the officer or manager in charge. If it’s just you, leave it blank.

Contact Details (Sections 4–8)

Here, give your address and phone number.

- Use your current mailing address. If you moved recently, also update your address with the IRS separately using the IRS address change online.

- Add a number you answer. Sometimes the IRS will call instead of mailing.

Lien Information (Section 9)

This is where you identify the lien.

- Best: Attach a copy of the lien notice.

- If you don’t have it: Write the lien serial number, filing date, and recording office.

That’s how the IRS matches your request to the right record.

Lien Status (Section 10)

Pick the current status:

- Open: You still owe a balance.

- Released: The lien is satisfied or unenforceable.

- Unknown: If you’re not sure.

Even if it’s “Released,” you can still use Form 12277 to pull the notice from public files.

Reason for Withdrawal (Section 11)

You’ll see five checkboxes, each tied to the law under section 6323(j). Choose the one(s) that applies. If your lien is already released, the IRS suggests checking the “best interest” box.

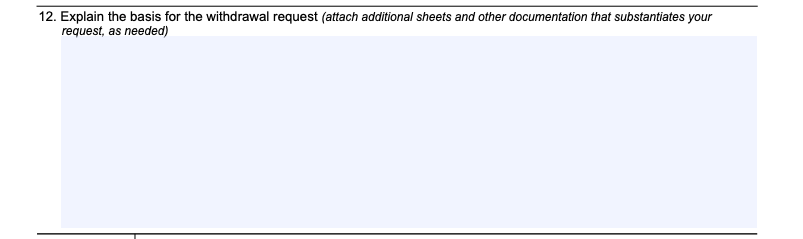

Your Story (Section 12)

This is your chance to explain. Keep it short and back it with proof.

- State your situation: “I am in a Direct Debit Installment Agreement.”

- Link to a reason: “The IRS rules allow withdrawal for direct debit taxpayers.”

- Explain the benefit: “Withdrawing the lien helps me refinance, ensuring steady payments.”

Use an extra sheet if needed.

Signature and Affirmation

At the bottom, you sign under penalties of perjury. This means you’re swearing your statement is true.

- Individual: Just sign and date.

- Business: Sign and include your title (like Owner, Manager, or CFO).

Application Process

Here are the five application steps you should follow before and after filing IRS Form 12277.

Gather Supporting Documentation

Pull together what proves your reason:

- Copy of the lien notice (Form 668(Y)), or the serial number, filing date, and recording office if you lack the copy.

- Proof of your Direct Debit plan or other payment plan, if that is your reason.

- Letters that show a withdrawal help collection: a loan pre-approval, an employment letter, a lease application, or a licensing notice.

Fill-Out Form 12277

Follow the step-by-step process that was given in the above section to fill the Form 12277.

Attach Supporting Documentation

Attach copies, not originals. If you want the IRS to notify lenders or credit agencies after approval, include a simple letter that lists each company name and address. The IRS can send those notices if you ask in writing; your request is the IRS’s authority to share the withdrawal.

Where to File?

Mail your application to the IRS office that has your account, if you know it. If you do not know, mail it to “IRS, ATTN: Advisory Group Manager,” where you live or where the business is based.

You can also use Publication 4235 to find the right Advisory address. Put your phone number on the cover page in case a reviewer needs a quick answer.

What to Expect After Submission?

After you send IRS Form 12277, the IRS reviews your request. Two things can happen:

- Approval: The IRS records the withdrawal (Form 10916(c)) where the lien was filed and mails you a copy. If you ask in writing, it will also notify credit bureaus or lenders.

- Denial: You’ll get a letter explaining why, along with your right to appeal. Often, adding more proof or choosing the right reason allows you to reapply.

In most cases, you either walk away with an official withdrawal on file or clear guidance on what to fix. That’s the path to real IRS lien removal from the public record.

Problems and Solutions

Even though IRS Form 12277 is short, small mistakes can sink your request. Here are the most common problems people run into and how to fix them before mailing.

| Problem | Fix |

| Missing lien details | Attach the lien notice, or list the serial number, date, and filing office. |

| Wrong reason checked | Match your reason to proof (e.g., Direct Debit plan → attach bank drafts). |

| Lien already paid, but still showing | Check “best interest” to withdraw the old released notice. |

| Sent to the wrong office | Use IRS Publication 4235 for the correct Advisory address. |

| Credit bureaus not updated | Include a written list of lenders/credit agencies to notify. |

| Denial letter | Add stronger proof or choose a better reason, then reapply or appeal. |

| No supporting docs | Keep Section 12 short and attach labeled evidence. |

| Business signer error | Add your title when signing for a business. |

| Mixing “withdrawal” and “release” | Withdrawal clears the public notice; release ends the lien itself. |

When to Seek Professional Help?

Call for help if your case touches more than one issue at once. Here are common signs:

- You owe across many years and also need a payment plan.

- You must sell or refinance a property fast.

- Your license, contract, or job offer is on the line, and you need the right reason with the right proof.

- You are not sure whether a withdrawal, a release, or a discharge solves your problem.

Rebuild Credit Now with Hopkins CPA Firm

Clearing a tax lien notice from public records is possible with IRS Form 12277, and knowing how to file it the right way can protect your credit and open financial doors again.

Hopkins CPA Firm is the best choice to handle Form 12277. We prepare the form, gather proof, speak with the IRS, and strengthen your case for approval. Our team knows how to speed up results and solve tax debt issues beyond liens. Let us help you move forward with confidence. Contact us today to get started.